| Category | Details |

|---|---|

| Topic | GLP-1 weight loss drugs — insurance coverage gaps and alternative financing options in 2026 |

| Key Figures | 50%+ of employer plans exclude weight loss GLP-1s; out-of-pocket cost: $900–$1,400/month; 15M+ US adults prescribed GLP-1s in 2025 |

| Who It Affects | Patients with obesity or overweight conditions seeking prescription weight loss treatment; employers; insurers; pharmaceutical manufacturers |

| Time Period | 2026 plan year — open enrollment decisions and coverage changes taking effect now |

| Bottom Line | Even without insurance, several practical options exist to access GLP-1 medications at lower costs, but they require research, persistence, and careful financial planning. |

When Insurance Says No to Weight Loss Drugs — What You Can Do in 2026

You finally get a prescription for one of the breakthrough GLP-1 weight loss medications. You walk to the pharmacy feeling hopeful. Then the pharmacist tells you the price: over a thousand dollars for a month’s supply, because your insurance plan does not cover it. This scene has played out millions of times across the United States, and in 2026, it is still one of the most frustrating financial barriers in healthcare. The GLP-1 weight loss insurance 2026 landscape remains uneven — some plans cover these drugs, many do not, and the ones that do often come with strict pre-authorisation requirements, step therapy rules, or high out-of-pocket costs. This article is a practical guide for anyone facing a denial. We will walk through the numbers, explain why coverage gaps persist, and lay out realistic options — from manufacturer savings programmes to compounding pharmacies and strategic insurance choices — so you can make an informed financial decision about your health.

Why Your Insurance Probably Won’t Pay

GLP-1 receptor agonists were originally developed to treat type 2 diabetes. Drugs like semaglutide (Ozempic, Wegovy) and tirzepatide (Mounjaro, Zepbound) proved so effective at promoting weight loss that demand exploded. By 2025, more than 15 million adults in the United States had received a prescription for one of these medications, according to IQVIA data. But health insurance coverage has not kept up with demand.

The core issue is cost. GLP-1 drugs carry list prices between $900 and $1,400 per month before insurance. Employers and insurers are hesitant to add these medications to formularies because the potential patient population is enormous — over 40% of American adults have obesity — and covering them all would dramatically raise premiums. A 2024 survey by the International Foundation of Employee Benefit Plans found that only 44% of large employers and 20% of small employers included weight loss GLP-1s in their prescription drug plans. Those numbers have shifted only modestly in 2026. Many plans that do offer coverage require patients to fail cheaper alternatives first, a process known as step therapy. Others cap coverage at six or twelve months. The result is that the GLP-1 weight loss insurance 2026 environment is fragmented, confusing, and expensive for the average patient.

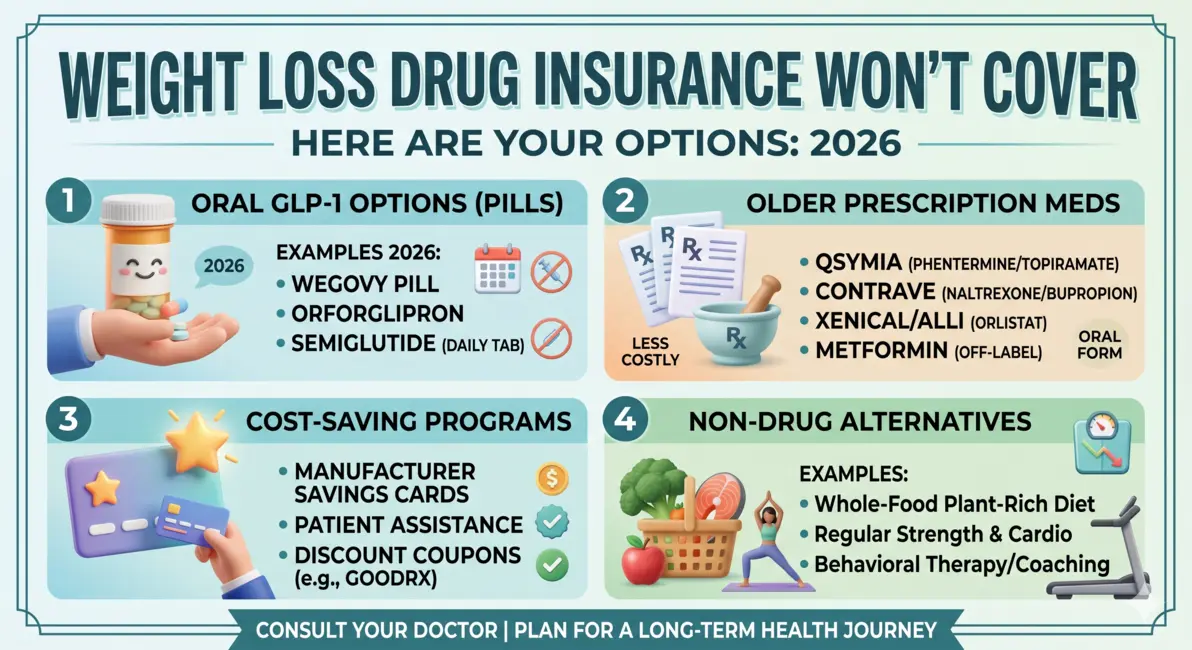

Your Options When Insurance Won’t Cover

Manufacturer Savings Cards and Patient Assistance Programmes

Both Novo Nordisk (the maker of Wegovy and Ozempic) and Eli Lilly (the maker of Zepbound and Mounjaro) offer savings cards that can reduce the monthly cost for eligible patients. In 2026, these cards typically bring the price down to around $200 to $500 per month for patients with commercial insurance that does not cover the drug. For patients without any insurance, manufacturer patient assistance programmes may offer the medication at no cost if your household income falls below a certain threshold — generally 400% of the federal poverty level. The application process can be time-consuming, but for those who qualify, it is the most affordable route. You can find these programmes on the official manufacturer websites. Be aware that the cards cannot be used with government insurance plans like Medicare or Medicaid due to federal anti-kickback rules.

Compounding Pharmacies and Generic Alternatives

Compounded semaglutide and tirzepatide have become increasingly popular alternatives for patients who cannot access brand-name drugs through insurance. Compounding pharmacies produce custom versions of these medications, often at a fraction of the retail price — typically $150 to $350 per month. However, this option comes with important caveats. Compounded drugs are not reviewed by the FDA for safety, efficacy, or quality. In 2024 and 2025, the FDA issued several warning letters about compounded GLP-1 products linked to adverse events. If you choose this route, use a pharmacy that is accredited by the Pharmacy Compounding Accreditation Board (PCAB) and requires a valid prescription from your doctor. Also note that some compounding pharmacies are now shipping lower-cost vials of branded Zepbound directly to patients through Eli Lilly’s direct-to-consumer platform, which launched in late 2025 and expanded in 2026, offering a 2.5 mg vial for about $399 per month.

Strategic Insurance Choices and Appeals

If you are self-employed or choosing a plan during open enrollment, you can research which plans cover weight loss GLP-1s in your state. The Affordable Care Act marketplace does not require plans to cover weight loss medications, but some do. You can filter plans by prescription drug coverage during enrollment. For those with employer-sponsored insurance who receive a denial, filing an appeal with your insurance company is a legitimate and often underused option. Your doctor can write a letter of medical necessity explaining why the drug is needed and why alternatives were ineffective or contraindicated. Data from the Kaiser Family Foundation shows that about 40% of initial denials are overturned on appeal. It takes time and persistence, but it costs nothing to try.

Key Points

- More than half of employer-sponsored insurance plans in 2026 still do not cover GLP-1 medications specifically for weight loss, leaving patients with monthly costs of $900–$1,400.

- Manufacturer savings cards from Novo Nordisk and Eli Lilly can reduce out-of-pocket costs to $200–$500 per month for patients with commercial insurance that excludes coverage.

- Compounded semaglutide and tirzepatide from accredited pharmacies offer a lower-cost alternative ($150–$350/month), but they are not FDA-approved, so caution is essential.

- Eli Lilly’s direct-to-consumer programme now offers branded Zepbound vials for around $399 per month, providing a safe middle-ground option for self-pay patients.

- Filing a formal insurance appeal with supporting medical documentation from your doctor overturns roughly 40% of initial coverage denials — a free option worth pursuing.

What This Means for Patients and the Market

The GLP-1 weight loss insurance 2026 landscape is a reflection of a larger struggle between pharmaceutical pricing, insurance economics, and patient demand. In the short term, patients are caught in the middle. Those who can afford to pay out of pocket or who qualify for assistance programmes have access; those who cannot are left with few good options. This disparity is creating a two-tiered system where financial resources, not medical need, determine who gets treatment.

Looking ahead, several forces could shift the balance. The patent on semaglutide is expected to expire later this decade, opening the door for lower-cost generic versions that could dramatically reduce prices. Several state legislatures are considering bills that would require insurance plans to cover obesity medications, and Medicare is currently reviewing whether to add weight loss GLP-1s to Part D coverage — a decision that, if approved, could reshape the entire market. For now, the most effective strategy for patients is a combination of research, advocacy, and financial planning. Compare plans during open enrollment, apply for manufacturer discounts, consult your doctor about alternatives, and do not accept a denial as final.

People Also Ask

Don’t Let a Denial Be the Final Word

If your insurance plan does not cover GLP-1 weight loss medications in 2026, you are far from alone — and you are far from out of options. The GLP-1 weight loss insurance 2026 environment is challenging, but patients who take an active role in researching their options can still find a path forward. Start with the manufacturer savings cards, explore accredited compounding pharmacies if budget allows, check whether your employer is willing to add coverage during the next contract negotiation, and always file an appeal if you receive a denial. Your doctor can be your strongest ally in that process. The financial and healthcare systems are slow to change, but your health does not have to wait. If you found this guide helpful, share it with someone who might be struggling with the same decision. Knowledge is the most affordable prescription of all.

This article is for informational and educational purposes only and does not constitute medical or financial advice. Always consult your healthcare provider before starting any medication and your insurance provider for coverage details specific to your plan.

Sources: IQVIA National Prescription Audit, International Foundation of Employee Benefit Plans 2024–2025 Survey, Kaiser Family Foundation, FDA compounding pharmacy advisories, Novo Nordisk and Eli Lilly patient assistance programme data.